Finding the right home loan can feel confusing, especially in a competitive market like Florida. If you’re searching for your first house or thinking about upgrading, you’ve probably seen the debate: FHA vs Conventional Loans in Florida: Which Is Better? Many buyers struggle to decide which is the smarter choice. Lenders, real estate agents, and even friends often give different advice. Your decision really matters—it can save you thousands of dollars, affect your approval chances, and even shape your future finances.

Let’s break down FHA and conventional loans in Florida. We’ll look at the basics, see how they compare, and uncover important details many people miss. By the end, you’ll know which loan is better for your needs, budget, and goals.

Understanding Fha Loans In Florida

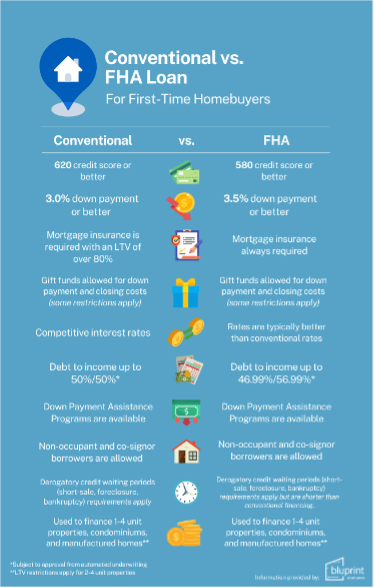

FHA loans are mortgages insured by the Federal Housing Administration. They are popular with first-time buyers and people who have lower credit scores. In Florida, many buyers pick FHA loans because of the flexible requirements.

Key Benefits Of Fha Loans

- Low down payment: Usually only 3.5% of the home’s price.

- Easier credit approval: You may qualify with a credit score as low as 580.

- Flexible debt-to-income ratios: Lenders can accept higher monthly debts.

- Assumable loans: If you sell your house, the next buyer can take over your FHA loan. This can be a big advantage if interest rates rise.

Important Fha Loan Limits In Florida

Every county in Florida has maximum loan limits for FHA loans. In 2024, most counties have a limit of $498,257 for single-family homes, but some high-cost areas go up to $621,000 or more. Always check your county’s limit before applying.

Fha Mortgage Insurance

FHA loans require two kinds of mortgage insurance:

- Upfront Mortgage Insurance Premium (UFMIP): 1.75% of the loan, paid at closing (often added to your loan amount).

- Annual Mortgage Insurance Premium (MIP): Paid monthly. This usually lasts for the life of the loan unless you refinance to a conventional loan.

Who Should Consider An Fha Loan In Florida?

- Buyers with credit scores under 700

- People with limited savings for a down payment

- Those with higher monthly debts

- Anyone with a short or spotty credit history

What Are Conventional Loans?

Conventional loans are not insured by any government agency. They follow rules set by Fannie Mae and Freddie Mac. In Florida, these loans are common for buyers with good credit and higher incomes.

Key Benefits Of Conventional Loans

- No upfront mortgage insurance required

- Private mortgage insurance (PMI) can be removed once you reach 20% equity

- Higher loan limits than FHA, especially for luxury homes

- Often lower total costs over the life of the loan if you qualify for good rates

Conventional Loan Requirements In Florida

- Credit score: At least 620, but 740+ gets the best rates

- Down payment: As low as 3% for some buyers, but 5% or more is common

- Debt-to-income ratio: Usually not higher than 43%

- Stable income and employment history

Who Should Consider A Conventional Loan In Florida?

- Buyers with strong credit (700+)

- Those with a larger down payment

- Homeowners looking for lower long-term costs

- Anyone buying homes above FHA limits

Fha Vs Conventional Loans In Florida: Key Differences

Understanding the main differences is critical for making the right choice. Here’s a clear comparison:

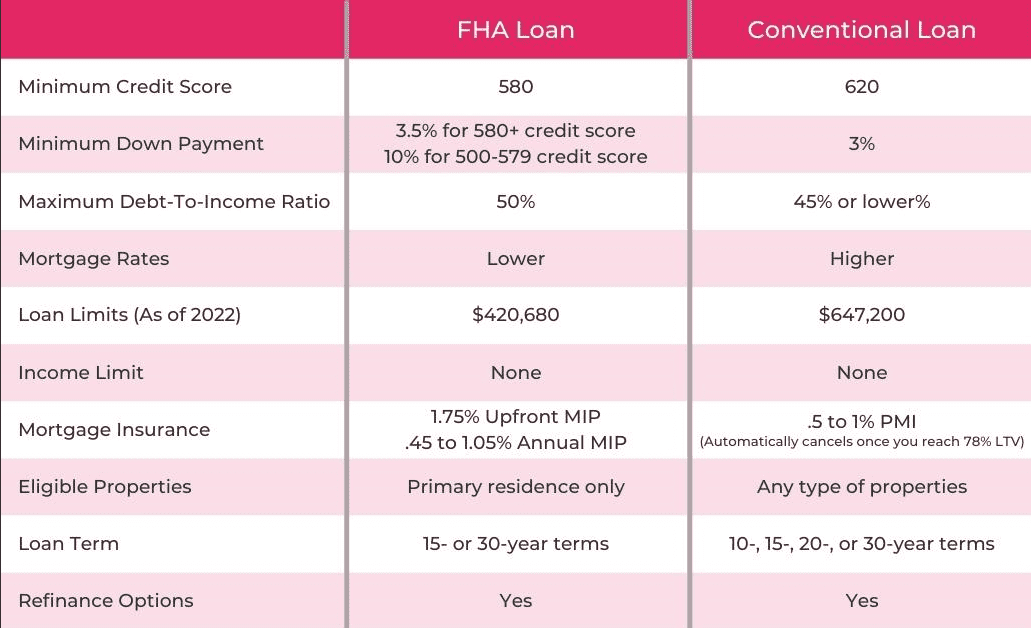

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Credit Score | 580 (3.5% down) | 620 (often 700+ for best rates) |

| Minimum Down Payment | 3.5% | 3%-5% |

| Mortgage Insurance | Required (UFMIP & MIP) | PMI if <20% down, removable |

| Loan Limits (2024) | $498,257 – $621,000+ | $766,550 (standard), higher in some areas |

| Assumable | Yes | No |

| Best For | First-time, low credit, small down payment | Good credit, larger down payment |

Fha Vs Conventional Loans In Florida: Costs And Payments

A big deciding factor is how much you’ll pay. Let’s break down the costs.

Down Payment Comparison

- FHA: 3.5% minimum, so on a $400,000 home, that’s $14,000.

- Conventional: 3%-5% minimum, so $12,000–$20,000 on the same home. But lower down payments mean higher PMI.

Mortgage Insurance Costs

For FHA loans, mortgage insurance is required no matter how much you put down. For conventional loans, PMI can be dropped after you build 20% equity.

For example, on a $350,000 home:

- FHA monthly MIP: About $200 (varies by loan size and down payment).

- Conventional PMI: Around $150, but could be less with good credit. Once you reach 20% equity, PMI can be removed, saving you money each month.

Interest Rates

FHA loans often have slightly lower rates for buyers with less-than-perfect credit. Conventional loans give the best rates to buyers with high credit.

Closing Costs

Both loans have closing costs (usually 2%-5% of the home price), but FHA loans have the extra upfront MIP. You can often ask the seller to pay some closing costs, especially with FHA.

Credit: www.southeastfg.com

Fha Vs Conventional Loans In Florida: Approval Process

Getting approved can be different for each loan type.

Fha Loan Approval Steps

- Pre-approval: Lender reviews your credit, income, and debts.

- Find a home: Make an offer and sign a contract.

- Appraisal: FHA requires a strict appraisal for safety and value.

- Final approval: Lender checks all documents and gives final OK.

- Closing: Sign papers, pay costs, get your keys.

Conventional Loan Approval Steps

- Pre-approval: Similar review, but lenders may be stricter on credit.

- Find a home: Make an offer, sign a contract.

- Appraisal: Less strict than FHA, but still required.

- Final approval: Lender checks income, credit, and down payment.

- Closing: Finish paperwork and payments.

Non-obvious insight: Many buyers don’t realize that FHA appraisals are tougher. The property must meet government safety rules. This can cause delays if repairs are needed before closing.

Fha Vs Conventional Loans In Florida: Pros And Cons

It’s smart to weigh all the positives and negatives.

Fha Loan Pros

- Easier to qualify with low credit

- Low down payment

- Can get help with closing costs

- Assumable loan can help if you sell in the future

Fha Loan Cons

- Mortgage insurance for the life of the loan (unless you refinance)

- Loan limits may not cover higher-priced homes

- Tougher property standards may delay closing

Conventional Loan Pros

- No mortgage insurance after 20% equity

- Higher loan limits for expensive homes

- More flexible property standards

- Lower long-term costs if you qualify for good rates

Conventional Loan Cons

- Harder to qualify with low credit

- Higher down payment may be needed

- PMI can be expensive with low credit and low down payment

Which Is Better For Florida Homebuyers?

The answer depends on your credit score, down payment, income, and the price of the home you want. Here’s a quick guide:

| You Should Choose | If You… |

|---|---|

| FHA Loan |

|

| Conventional Loan |

|

Non-obvious insight: If you plan to keep your home for only a few years, the difference in mortgage insurance may not matter as much. But if you plan to stay long-term, conventional loans often save more money over time because you can drop PMI.

Important Tips When Choosing Fha Or Conventional Loans In Florida

- Check your local loan limits. Some Florida counties have higher limits, especially near big cities or popular coasts.

- Compare rates from at least three lenders. Each lender can offer different terms, especially on mortgage insurance.

- Calculate both upfront and total long-term costs. Don’t just look at monthly payments.

- Ask about seller-paid closing costs. FHA allows sellers to pay up to 6% of the price, while conventional loans allow 3%-6% (depending on your down payment).

- Look at your future plans. If you plan to move or refinance soon, initial costs matter more. If you plan to stay, focus on long-term savings.

- Consider how fast you can build equity. The faster you reach 20% equity, the sooner you can remove PMI from a conventional loan.

Credit: bluprinthomeloans.com

How Florida’s Market Affects Your Loan Choice

Florida’s real estate market is unique. Prices are rising in many areas, and competition is high. Many homes sell quickly, and sellers may prefer buyers with conventional loans. This is because FHA loans can require more inspections and repairs.

But don’t let this stop you from choosing FHA if it fits your needs. Many buyers succeed with FHA loans, especially in less competitive markets or with patient sellers.

Real-world Example: Fha Vs Conventional In Florida

Maria wants to buy a $350,000 home in Miami. Her credit score is 660, and she has $15,000 for a down payment.

- FHA loan: She qualifies easily, puts down 3.5% ($12,250), pays mortgage insurance, and gets a rate of 6.3%.

- Conventional loan: She needs at least 5% down ($17,500) and gets a higher rate because her credit is below 700. Monthly PMI is higher, and approval is harder.

For Maria, FHA is the better choice. But if her score was 720 and she had more savings, a conventional loan would be cheaper in the long run.

Get Professional Help

Choosing between FHA vs conventional loans in Florida is a big decision. There are many details, and one small mistake can cost you money or cause delays. Speaking with a local expert can help you compare your options and find the best fit for your needs.

Ready to take the next step? Contact us for a free, no-pressure loan consultation. Call +1 (706) 844-3723 or email info@enriquebello.com. We’ll help you compare FHA and conventional loans in Florida and answer your questions.

For more details on FHA and conventional loan rules, visit the Consumer Financial Protection Bureau.

Frequently Asked Questions

What Is The Main Difference Between Fha And Conventional Loans In Florida?

The main difference is that FHA loans are backed by the government and have easier requirements for credit scores and down payments. Conventional loans are not government-backed and usually require higher credit scores but can have lower long-term costs if you qualify.

Can I Switch From An Fha Loan To A Conventional Loan Later?

Yes, you can refinance your FHA loan into a conventional loan. Many Florida homeowners do this to get rid of FHA mortgage insurance once they build enough equity or improve their credit.

Do Sellers In Florida Prefer Fha Or Conventional Buyers?

Many sellers prefer conventional loan buyers because the process can be faster and usually requires fewer repairs. However, FHA buyers can still get accepted, especially with good offers and patient sellers.

How Can I Get Rid Of Mortgage Insurance On My Loan?

With conventional loans, you can remove PMI when you reach 20% equity. With FHA loans, mortgage insurance lasts for the life of the loan unless you refinance to a conventional loan.

How Do I Know Which Loan Is Better For Me In Florida?

Look at your credit score, down payment savings, and the price of the home you want. Compare the total costs, not just the monthly payments. Speak with a local lender or contact us at +1 (706) 844-3723 or info@enriquebello.com for a free review of your options.

Don’t wait—get expert advice now and make your Florida home dreams come true!

Credit: www.ebenezermortgage.com