Are you searching for a way to build wealth, enjoy steady returns, and help others achieve their dreams? Learning how to become a private money lender in Florida could be your perfect opportunity. In recent years, private lending has become a popular investment strategy. Many Florida residents are turning their capital into reliable income streams by financing real estate deals or small businesses. If you want to join this movement, understanding the process, legal requirements, and best practices is essential. This guide explains every step, shares insider tips, and helps you avoid common mistakes. By the end, you’ll know how to start, grow, and protect your lending business the right way.

What Is Private Money Lending?

Private money lending means individuals—like you—lend their own money to other people or businesses, usually for real estate investments. Unlike banks, private lenders can offer faster approvals and flexible terms. In Florida, this is a thriving market, especially for fix-and-flip properties and small business growth.

Why Consider Becoming A Private Money Lender In Florida?

The Sunshine State offers unique advantages for private lenders. Florida’s booming real estate market and strong rental demand create a constant need for financing. As a private lender, you can earn higher interest rates than traditional investments and diversify your portfolio. Also, you help borrowers who may not qualify for bank loans, making a real difference in their lives.

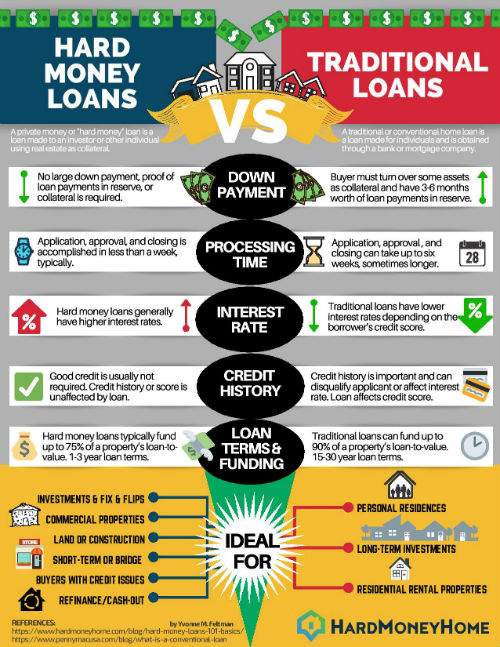

:max_bytes(150000):strip_icc()/hard-money-basics-315413_Final-cdfb8155170c4becb112da91bd673fe8-0472b1f57ff94abebddef246c221a65f.jpg)

Credit: www.thebalancemoney.com

Steps To Become A Private Money Lender In Florida

1. Understand Florida’s Lending Laws

Florida has specific rules for private lenders. You must comply with state usury laws, licensing requirements, and consumer protection guidelines. For most real estate loans, you do not need a banking license. However, lending to more than one person or company, or making consumer loans, may require registration with the Florida Office of Financial Regulation. Always consult a legal expert to ensure compliance.

2. Build Your Capital Base

To start lending, you need money to lend. Most private lenders use personal savings, home equity, retirement accounts, or funds from other investors. The more capital you have, the more deals you can fund. Many successful lenders start small—sometimes with as little as $50,000—and grow over time.

3. Decide Your Lending Model

There are different ways to lend money:

- Direct lending: You make loans directly to a borrower.

- Partnering with brokers: You work with real estate agents or mortgage brokers to find deals.

- Lending through funds: You join or start a private lending fund with other investors.

Each model has pros and cons. Direct lending gives you full control, but more responsibility. Partnering with brokers can help you find better deals but may reduce your profits.

4. Choose Your Loan Types

Most private lenders in Florida focus on these loan types:

- Fix-and-flip loans for investors buying, renovating, and selling homes.

- Buy-and-hold loans for rental property investors.

- Bridge loans for short-term financing until permanent financing is available.

- Business loans for small companies needing quick cash.

Decide which market you want to serve. Study typical loan sizes, terms, and risks. For example, fix-and-flip loans are short-term and high-interest, while buy-and-hold loans are longer and lower-risk.

5. Set Your Lending Criteria

To protect your investment, define who you will lend to and on what terms. Key criteria include:

- Loan-to-value (LTV) ratio: Most lenders keep LTV below 70% to reduce risk.

- Borrower’s experience: Prefer borrowers with a good track record.

- Property type and location: Focus on areas you know and trust.

Create a checklist for every deal. This keeps your process consistent and safe.

6. Structure Your Loans Properly

A strong loan agreement protects you and the borrower. Work with a Florida attorney to draft your documents. Key elements include:

- Interest rate and payment schedule

- Term length

- Collateral (usually real estate)

- Default and foreclosure terms

- Fees and penalties

Never skip legal paperwork. A simple mistake can cost you thousands.

7. Secure Your Investment

In Florida, private lenders usually secure their loans with a mortgage or deed of trust recorded on the property. This means if the borrower defaults, you have the right to take the property through foreclosure. Always verify the property’s title is clear and free of other claims.

8. Evaluate Borrowers And Properties

Successful private money lenders never skip due diligence. Check:

- Credit reports and background checks

- Property appraisals

- Title insurance

- Borrower’s exit plan (how they will pay you back)

Many new lenders forget to ask about the exit strategy. If the borrower cannot refinance or sell, you may be stuck with the property.

9. Set Up Your Business Legally

Operate as a limited liability company (LLC) or other legal entity. This protects your personal assets from lawsuits. Register your business with the State of Florida and get an EIN (Employer Identification Number) from the IRS.

10. Build Your Network And Reputation

Relationships matter. Connect with real estate agents, attorneys, title companies, and other lenders. Join local real estate investment groups. A strong network brings you more deals and helps you spot risks early.

The Florida Private Lending Process: What To Expect

Each loan follows a clear process:

- Deal sourcing: Find borrowers through referrals, networking, or advertising.

- Application review: Analyze loan requests and run background checks.

- Due diligence: Inspect the property, verify value, and check legal documents.

- Loan structuring: Finalize terms and sign agreements.

- Funding: Transfer money to the borrower, usually through a closing agent.

- Servicing: Collect payments, manage escrow, and track loan performance.

- Exit: Get repaid or start foreclosure if necessary.

Here’s a quick comparison of traditional vs. private lending in Florida:

| Feature | Traditional Bank Loan | Private Money Loan |

|---|---|---|

| Approval Time | 30–60 days | 3–10 days |

| Credit Score Needed | High (700+) | Flexible |

| Loan Term | 15–30 years | 6–24 months |

| Interest Rate | 4–7% | 8–15% or more |

Credit: www.hardmoneyhome.com

Key Legal And Tax Considerations For Florida Private Lenders

Know The Usury Laws

Florida limits the maximum interest you can charge—usually 18% for loans under $500,000 and 25% for larger loans. Charging above this is illegal and can result in fines or loss of your loan.

Get Proper Licensing

You usually don’t need a lender license for business-purpose loans secured by real estate, but consumer loans and high-volume lending may require registration. Always check with the Florida Office of Financial Regulation.

Understand Taxes

Interest income from private lending is taxable. Work with a CPA who understands private lending. Some lenders use self-directed IRAs for tax benefits.

Risks And How To Manage Them

Every investment has risks. Private lending is no different. The biggest dangers are:

- Default risk: The borrower fails to pay you back.

- Property value drops: Your collateral may not cover your loan.

- Legal issues: Poor contracts or title problems can cost you.

Here’s how to reduce your risk:

| Risk | Prevention Tip |

|---|---|

| Default | Keep LTV below 70%, verify borrower’s plan |

| Title Issues | Get title insurance and use a real estate attorney |

| Market Downturn | Lend only on properties in stable areas |

Growing Your Private Lending Business In Florida

Once you’ve closed your first few loans, you may want to expand. Consider these strategies:

- Reinvest profits to fund more deals.

- Partner with other investors to pool resources.

- Automate loan servicing with software tools.

- Market your services through real estate groups and online platforms.

Stay up to date with market trends. For example, short-term rentals are growing in parts of Florida, creating new lending opportunities.

Common Mistakes New Private Lenders Make

Many beginners lose money by:

- Skipping due diligence: Always verify the borrower and property.

- Ignoring legal advice: Saving money on lawyers is expensive later.

- Overvaluing properties: Get third-party appraisals.

- Lending to friends or family: Treat every loan professionally.

One insight beginners miss: Always ask how the borrower will pay you back, not just “if” they can. If the plan is not clear, walk away.

Another often-overlooked tip: Document every step. Keep records of emails, agreements, and payments. This protects you if there’s a dispute.

Real Success Stories: Florida Private Lenders In Action

Sarah, a Tampa retiree, started with $100,000. She focused on short-term fix-and-flip loans. By staying under 65% LTV and using strong contracts, she averaged 10% returns for three years. When one borrower defaulted, Sarah’s lien on the property let her recover her money in foreclosure.

John, a Miami small business owner, lent to buy-and-hold investors. He partnered with a real estate attorney and hired a loan servicer. John’s network brought him steady deals, and he avoided losses by sticking to his criteria.

Helpful Resources For Aspiring Private Lenders

If you want to dive deeper, check out the following:

- Florida Office of Financial Regulation: Rules and licensing info

- BiggerPockets: Forums and guides on private lending

- American Association of Private Lenders: Education and networking

For an in-depth overview of private money lending, visit this Wikipedia article.

Ready To Start Your Private Lending Journey?

Becoming a private money lender in Florida is a powerful way to grow your wealth and help your community. The steps are clear: learn the rules, build your capital, choose your deals carefully, and protect your investment. The process is not risk-free, but with smart planning, you can earn strong returns while minimizing dangers. If you want to learn more or need expert guidance, reach out to us at +1 (706) 844-3723 or info@enriquebello.com. Start your journey and unlock new financial possibilities today!

Frequently Asked Questions

What Is The Minimum Capital Needed To Become A Private Money Lender In Florida?

There’s no legal minimum, but most lenders start with at least $50,000. More capital allows you to fund larger or multiple deals, but you can begin small and grow as you gain experience.

Do I Need A License To Lend Money Privately In Florida?

For most business-purpose or real estate-secured loans, you do not need a lender’s license. If you make consumer loans or lend at high volume, you may need to register with the Florida Office of Financial Regulation.

How Much Interest Can I Legally Charge On Private Loans In Florida?

Florida law usually allows up to 18% interest on loans under $500,000 and 25% on larger loans. Charging more is illegal and can void your loan.

What Happens If My Borrower Stops Paying?

If you have a mortgage or deed of trust, you can start foreclosure proceedings to recover your investment. Proper loan documents and title insurance are key to protecting your rights.

How Do I Find Good Borrowers For Private Loans?

Build your network in the real estate community, join investment groups, or work with trusted brokers. Always screen borrowers and properties carefully before lending.

Ready to take the next step? Call +1 (706) 844-3723 or email info@enriquebello.com for a personal consultation and start your private lending business in Florida today!

Credit: bradloans.com